MANM377 Cases in International Finance Case-2

The case report aims to evaluate your knowledge and skills related to international finance. You must choose one out of the three cases, analyse the case using relevant questions and submit a report. You must focus on the main question of your chosen case study and critically evaluate with/without the help of additional questions posed. It is crucial to apply financial principles when analysing the case. You can find related case documents under Assessment Information in our SL module page.

Main question: Critically analyse the article and answer this question:

Analyse the risk inherent in convertible securities as mentioned in the case.

Additional questions: Considerations of the following questions may help you answer the main question above:

1. Briefly mention the key features of convertible securities.

2. Discuss the utility of convertible securities in corporate financing.

3. Analyse risk underlying convertible securities for the issuer and investors.

4. Discuss specific risk in convertible securities issued in foreign currencies.

Main question: Critically analyse the article and answer this question:

Is cross listing always beneficial to the parties involved?

Additional questions: Considerations of the following questions may help you answer the main question above:

1. What are some of the benefits of cross-listing?

2. What are the reasons behind occurrence of the problem as mentioned in the article?

3. How can one solve the problem?

4. Clarify the conceptual frameworks/theoretical foundations related to the problem in hand and the solution?

Main question: Critically analyse the case and answer this question:

Is the offer price of R85 per share fair for Ellerine Holdings Limited (EHL)?

Additional questions: Considerations of the following questions may help you answer the main question above:

1. Calculate the fair value of EHL using net present value approach.

2. Discuss any relevant M&A concepts related to target valuation.

3. Discuss financial or any other form of synergies that EHL will enjoy post-acquisition.

4. Recommend a decision to accept, decline, or negotiate the offer.

Each report should have the following structure:

1. Title: You should include the title of the case with your student code - URN.

2. Introduction: You should describe the case, highlight the points which are important in your view and answer the main question briefly.

3. Main Analysis: You should provide your logical arguments here.

4. Conclusion: You should conclude the case, briefly summarize your main analysis and provide any future recommendations.

5. References: Please use Harvard referencing style to cite references.

Your report must not exceed 3,000 words in length (excluding the references). Your report will be marked based on the rubric provided at the end of this document.

Summarizing the case may not be necessary. Instead, select one side of the story. For instance, if the main question can be answered with a Yes or No, you must choose one of these options and provide logical explanations to support your choice. Keep in mind that all questions related to the case can be approached from various angles, and there are no definitive right answers. To facilitate a better analysis of the case, additional questions/issues are provided. It is your decision which of these subsidiary questions/issues you want to address. Your analysis of the main question holds more significance than your response to additional questions. Ensure that your logical arguments in the analysis are coherent. You can freely utilize any resources or pose additional questions/issues that you believe will contribute to a more in-depth analysis of the case.

Cross-listing, or listing a company's shares on multiple stock exchanges in different countries is the process of listing a company's shares on multiple stock exchanges has become increasingly prevalent in today's globalized financial markets. Businesses now have easier access to international capital markets particularly, listing shares on both a domestic market and a foreign exchange, which is often a U.S. exchange, is an ideal destination for businesses (Bris, Cantale and Nishiotis, 2005).

The number of international companies listed on the NASDAQ and New York Stock Exchange (NYSE) increased over the years. As of March 2023, the NYSE had a total of 578 international companies, while the figure for the NASDAQ was much higher, standing 864 international companies listed. This clearly demonstrate the number international firms listed on NASDAQ has increased significantly over the years Figure-1 (Statista, 2023).

Figure 1 Statista 2023

Cross-listing provides several benefits, including increased access to global capital markets, increased visibility and credibility, a diverse investor base, improved liquidity, and currency diversification (Diniz-Maganini et al. 2023). Pagano et al. (2002) discovered that companies with intentions to raise money, companies with rising global sales, and companies operating in high-tech industries all have a tendency to cross-list in the US. However, it is essential to understand that cross-listing has its own unique set of difficulties in addition to its advantages. According to different studies (Koh et al., 2013) the regulatory and compliance burden, possible differences in reporting requirements across exchanges, operational and legal concerns, and the substantial expenses involved with cross-border listings are some issues that firms operating in various countries face. This report investigates the debate over whether or not cross-listing is always beneficial and discusses the complexities that must be considered.

This report also provide a thorough analysis of cross-listing benefits and drawbacks in the light of article: Holding foreign insiders accountable, stressing that the decision to cross-list should be based on the unique characteristics of each firm, their long-term objectives, and their internal resources for handling the complexities of international stock exchanges. One can get a more nuanced picture of whether or not cross-listing is advantageous for all parties involved if we consider the intricacies and possible downsides alongside the rewards.

The increased regulatory and compliance burden cross-listing places on corporations is a common argument against its widespread benefits (Sarkissian and Schill, 2016). Cross-listed companies must deal with the reporting, disclosure, and compliance obligations in the country they are listed. Furthermore, complying with these regulations may be difficult, time-consuming, and expensive. In particular, smaller businesses may find it difficult to set aside the resources they need to handle these regulatory problems properly (Temouri et al . 2016). Therefore, the advantages of cross-listing may be outweighed by the regulatory complexity, making it a less desirable alternative for certain businesses.

There is also the possibility of disparities in reporting across exchanges, which must be addressed when cross-listing (Lei et al.2023). Moreover, consistency and openness in financial reporting may be difficult for companies listed due to potential reporting standards and criteria variances. Thus making it difficult for investors and analysts to judge a company's financial health and performance with any degree of precision (Kamarudin et al. 2020). Therefore, value and viability of a business might be negatively affected by a lack of investor trust due to too complicated reporting.

In addition to this cross-listed companies face legal and jurisdictional issues since they operate in multiple countries. A company's activities and reputation in one jurisdiction may be adversely affected by legal conflicts, regulatory changes, or actions in another. As a result, understanding and managing these risks effectively requires substantial legal experience and resources (Esqueda, 2017). Hence, cross-listing might be more of a hindrance than an aid for businesses that aren't ready to handle these potential pitfalls.

Another consideration is cost effectiveness when calculating the total gain from cross-listing, because it entails expenditures such as listing fees, legal fees, continuing compliance costs, and the possibility of needing extra personnel to handle the complications of international listings (Dodd and Gilbert, 2016). These additional expenses may overshadow the advantages of cross-listing for smaller enterprises with limited financial resources. Therefore, some businesses may find cross-listing an unfeasible option due to the costs involved (Jackson Jr and Taylor, 2022).

Moreover, cross-listing might add layers of complexity and perhaps confuse investors. If investors have trouble buying and selling shares on several exchanges, it might slow down the market. This complexity can reduce shareholder value by influencing a company's stock price and liquidity (Ghosh and He, 2017). As an outcome it causes stock price volatility or lowers liquidity, investors may become confused or dissatisfied, negating such benefits.

On the other hand cross-listing has benefits, such as increased access to global capital markets, more visibility, a wider range of investors, better liquidity, and exposure to other currencies (Reiter, 2021). A company's choice to cross-list should be grounded on a thorough analysis of its current situation, long-term goals, and internal resources for handling the regulatory, compliance, operational, legal, and financial hurdles of international listings. Cross-listing may not be practical or beneficial for smaller organisations or those lacking the capacity to handle these complications efficiently (Diniz-Maganini et al. 2023). Therefore, viability of cross-listing as a strategy for any given business can only be determined after considering the advantages and disadvantages of the move.

Cross-listing provides several benefits to firms looking to increase their visibility and access to international capital markets.

3.1 Access to Global Capital Markets

Access to a broader pool of global investors and capital markets is one of the most significant benefits of cross-listing. A corporation may access a wider range of investors, including institutional investors, individual investors, and overseas funds, by listing on multiple markets (Sarkissian and Schill, 2016). More importantly, enterprises in developing markets or smaller economies may benefit greatly from cross-listing.

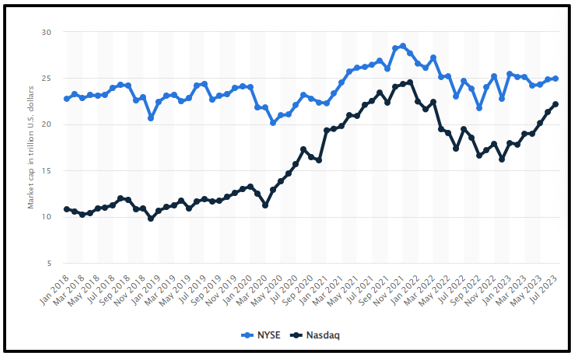

The two leading stock exchange in the United States New York Stock Exchange (NYSE) and the Nasdaq, have a combined market capitalization of $47 trillion as of July 2023 for listed businesses Fig- 2 (Statista.com, 2023). Thus companies may attract overseas investment and raise more capital than they could in their home market by listing on big international markets like the NYSE or the London Stock Exchange (LSE) (Jackson Jr and Taylor, 2022). Therefore, one of the most significant advantages of cross-listing is access to global stockholders and financial marketplaces.

Figure 2 Market Capitalisation of NYSE and Nasdaq (Source: Statista.com, 2023)

3.2 Enhanced Visibility and Credibility

Cross-listing on major international exchanges is equivalent to a seal of approval for businesses looking to establish themselves globally. This tricky manoeuvre does wonders for a company's seeking global profile and reputation (Temouri et al. 2016). A firm may successfully demonstrate its steadfast dedication to openness, strong corporate governance, and compliance with stringent international standards by participating in cross-listing.

Also, leading stock exchanges are strongly regulatory and reporting obligations provide a guiding light of trust for savvy investors. In the cutthroat world of global finance, companies that adhere to these prerequisites will be seen as reliable and trustworthy by their investors and customers (Lei et al.2023). In addition to this increased trust is useful for any business endeavour, but it's especially helpful for those aiming for global growth, deeper market penetration, or the formation of strategic partnerships. Moreover, cross-listing isn't just about the money; it's a strong indication of a company's commitment to excellence and readiness to satisfy the rigorous standards of the global business community (Jackson Jr and Taylor, 2022). Hence, broader range of investors, consumers, and partners are drawn in, creating long-lasting bonds based on trust and certainty.

3.3 Diversification of Investor Base

The strategic step of cross-listing allows businesses to increase their investor base across many locations, significantly benefiting risk management and market stability. Firms may protect themselves against economic downturns or geopolitical instability in their principal market by recruiting investors from various global markets (Kamarudin et al. 2020). But diversification of this base functions as a financial buffer, absorbing shocks and ensuring stability in the face of adversity.

Although a less diversified corporation is more susceptible to wild swings in stock price caused by market events or investor sentiment. However, broad investor base is a more stable stock price and it builds a solid structure that can weather the waves of the global economy (Chen et al. 2021).

Therefore, potential of cross-listing to promote investor diversity is a beneficial risk mitigation approach, giving firms more resilience in the face of market-specific issues and bolstering their position in the global marketplace.

3.4 Improved Liquidity

Liquidity, a cornerstone of the financial markets, is crucial for businesses and investors alike. Companies may significantly increase their liquidity via cross-listing, listing their shares on numerous international exchanges (Esqueda, 2017). This increase in market fluidity results from a larger pool of buyers and sellers operating across many time zones and regional markets.

Moreover, investors may easily buy or leave positions, increasing their opportunities for better pricing (Dodd and Gilbert, 2016). Further, increased liquidity benefits the market by narrowing the gap between the highest price a buyer is ready to pay and the lowest price a seller is willing to take, a crucial indicator known as the bid-ask spread which reduces the transaction costs for buyers and sellers resulted from a smaller bid-ask spread.

Cross-listing improves the trading ecosystem by giving businesses access to a broader investor base and giving investors the flexibility to move more easily and effectively within the market (Ghosh and He, 2017). Therefore, relevance of cross-listing in the financial sector is supported by the fact that it works hand in hand with liquidity.

3.5 Currency Diversification

One of another benefit of cross listing is that currency risk may be balanced out by the inherent liquidity provided as a result of cross-listing. As a result of being listed on various exchanges in different countries, a company's shares may be traded in various currencies (Reiter, 2021).

This results in company's financial performance may be less affected by currency fluctuations. For instance, the company's primary listing would be in the United States, but it would also be listed on the London Stock Exchange, so the company's shares could be traded in U.S. dollars and British pounds (Diniz-Maganini et al. 2023). As a result, company's profitability may be stabilised, and its susceptibility to currency rate fluctuations can be reduced if it diversifies into other currencies.

In short companies who want to increase their global reach and access international capital markets might benefit greatly from cross-listing. Additionally, increased access to capital, higher visibility and credibility, a diverse investor base, improved liquidity, and reduced currency risk are just a few benefits. While regulatory and compliance requirements are connected with cross-listing, the potential benefits often exceed the expenses, making it a desirable option for many organisations aiming to expand abroad.

4.1Exemption of Foreign Insiders from Reporting Requirements

This exemption was first created to encourage foreign firms to list on US exchanges. This exception, however, has been a cause for concern because of the dramatic growth in foreign listings, particularly from non-extradition nations like China and Russia (Temouri et al. 2016).

Figure-1 clearly demonstrate the number international firms listed on NASDAQ has increased significantly over the years (Statista, 2023).The article notes that the Section 16 reporting requirements do not apply to corporate insiders at foreign-domiciled businesses listed on US exchanges, which accounts for around 27% of all US-listed public corporations (Jackson Jr and Taylor, 2022). According to economic theory, opportunistic behaviour might increase as the chance of legal enforcement and sanctions reduces. Therefore, greater trade quantities and negative abnormal returns shown in their trades, especially in non-extradition nations, suggest possible abusive practices.

4.2 Lack of Public Scrutiny

The fact that non-U.S. nationals are exempted from Section 16 reporting requirements is a major contributor to the lack of public trust and company’s reputation. Compared to the reporting requirements for US insiders on Form 4, the reporting requirements for foreign insiders are less stringent (Lei et al.2023). This regulatory gap has prevented public scrutiny and openness on the trading activities of overseas corporate leaders. As a result, neither investors nor the general public know what drives these foreign insiders (Jackson Jr. and Taylor, 2022). The numbers presented in the article demonstrate that foreign insiders, on average, engage in far larger transactions than their US counterparts. According to the article, the average trade size of foreign insiders is roughly twice that of US insiders e.g. $6 million for the average foreign insider and $3 million for the average US insider. The average trading size of these foreign insiders affiliated with Russian and Chinese companies is around five times that of US insiders.

Foreign insiders have been able to operate with minimal oversight due to a lack of public disclosure laws, posing a danger to market integrity and investor confidence (Kamarudin et al. 2020). Therefore, regulatory exemption offered to foreign insiders has produced an imbalance in reporting requirements and inhibited transparency in their trading operations, which is a major contributor to the issue of a lack of public scrutiny.

4.3 Concerns about Opportunistic Trading

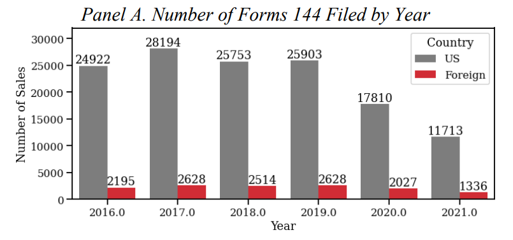

One of another concerns about the less stringent regulatory environment and the absence of effective enforcement mechanisms are in US is the heart of opportunistic trading by foreign insiders (Chen et al. 2021). According to Economic Theory, illegal activity is more likely to succeed when legal enforcement and sanctions are less likely. The situation worsens since certain foreign insiders, especially those from non-extradition nations like China and Russia, may believe they are immune to US law enforcement's pursuit (Esqueda, 2017). The article reveals that the SEC received approximately 147,000 paper Form 144s demonstrating over $500 billion in stock transactions, of them, 13,026 Form 144s were stock transactions by foreign insiders totalling $89 billion. The results further determined that 52% or $47 billion in stock transactions are attributed to foreign insiders affiliated with Chinese-companies listed on US exchanges. These results highlight the need for regulatory measures to address this issue and the concern about the opportunistic character of foreign insiders' trading activity.

Figure 3 Source- (Jackson Jr and Taylor, 2022)

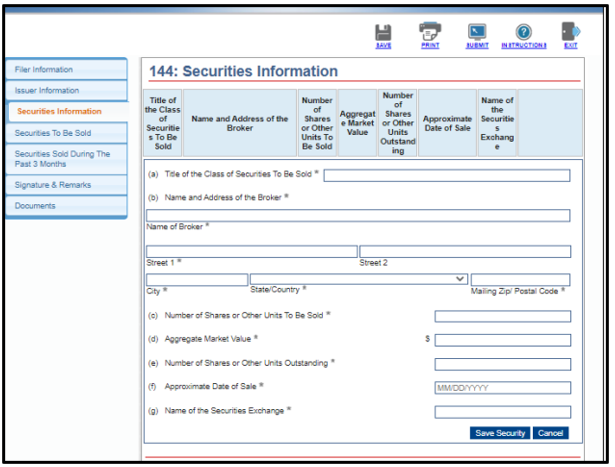

4.4 Limited Reporting via Form 144

In the past, mostly companies had to submit this form on paper, which presented several problems, including the fact that it was difficult for the general public to access. According to the article, the SEC's computerised public database, EDGAR, is missing most Form 144s since they were filed on paper. With the help of private data providers like The Washington Service, this has established a two-tiered disclosure system, with these files mainly available to major institutional customers (Diniz-Maganini et al. 2023). Thus, the issue of inadequate public scrutiny and market discipline is exacerbated by the fact that the broader investor community has restricted access to important information on the trading activity of foreign insiders (Jackson Jr and Taylor, 2022). However, SEC recently updated the filing procedure for Form 144, which foreign insiders use to report transactions of restricted securities subject to disclosure under alternative securities laws (Reiter, 2021).

Figure 2: Form 144

(Source:Sec.gov, 2022)

4.5 Abnormal Returns

The article presents strong evidence that these foreign insiders' typical stock sales, particularly those related to non-extradition nations, are associated with negative abnormal returns, with some examples indicating exceptionally considerable drops in company values (Ghosh and He, 2017). For instance stock sales were extraordinarily high and adverse: -18.8% in 12 months which is dependable with insiders trading more aggressively and the lack of extradition sheltering these insiders from US law enforcement.

4.6 Loss Avoidance by Insiders

The article quantifies the problem, suggesting that insiders affiliated with enterprises in non-extradition nations avoided $9 billion in damages throughout the sample period. This significant loss avoidance illustrates a disturbing trend in the trading behaviour of foreign business insiders, highlighting the need for more scrutiny and regulatory attention in this area (Temouri et al. 2016). According to the (Sarkissian and Schill, 2016), these insiders made trades to avoid major losses, suggesting an opportunistic and strategic approach. These significant loss avoidance strategies adopted by foreign insiders, especially those from non-extradition nations like China and Russia may result in loss of public confidence and scrutiny.

5.1 Reforming Reporting Requirements for Foreign Insiders

The exemption of foreign insiders from reporting requirements must be addressed, and authorities should look at both sides of the coin. It is critical to reevaluate and update these restrictions since the original exemption was designed to entice foreign firms to US exchanges (Chen et al. 2021). Moreover, transparency and market integrity might be improved by enforcing disclosure obligations on foreign insiders that are on par with those placed on US insiders under the current reporting system (Esqueda, 2017). This would promote fair and competitive markets by ensuring all investors have access to vital information, reducing the dangers of opportunistic behaviour.

5.2 Enhancing Foreign Insider Reporting Standards

Revisions to reporting requirements for foreign insiders are necessary to solve the problem of "Lack of Public Scrutiny." It is recommended to consider implementing a standardised reporting mechanism, like the Section 16 requirements for US insiders (Dodd and Gilbert, 2016). Furthermore, promoting openness by requiring foreign insiders to declare trades quickly using a defined form. In addition to this investors and the market may benefit from more transparency and understanding of the reasons for foreign insider trading by bridging the reporting gap between US and foreign insiders (Ghosh and He, 2017). This will lower the risk of opportunistic behaviour and increase market integrity and trust.

5.3 Strengthening Regulatory Oversight of Foreign Insiders

Regulatory authorities should strengthen enforcement mechanisms and transparency to address concerns about opportunistic trading by foreign insiders (Reiter, 2021). These measures may include increased surveillance of trading activity and tougher fines for insiders from non-extradition nations who do not comply. The SEC's Investor Advisory Committee believes expanding Section 16 reporting requirements to include foreign insiders may achieve a fair playing field and equal scrutiny (Diniz-Maganini et al. 2023). These rules are meant to discourage unethical trading practices, preserve market honesty, and safeguard investors' capital.

In conclusion, it's impossible to definitively say whether or not cross-listing is good for all parties. more access to global capital markets, more visibility, a broader investor base, higher liquidity, and lower currency risk are just a few of the many possible advantages of cross-listing. These benefits may be enormous and can contribute considerably to the development and success of many businesses, provided those businesses have the means and expertise to handle the difficulties of international listings. Cross-listing has its unique difficulties and risks, and this must be taken into account. Some organisations, especially those on a smaller scale, may not see a return on investment because of the high regulatory and compliance load, different reporting requirements, operational and legal risks, and high expenses.

In addition, the extra complexity of cross-listing may cause market inefficiencies and investor uncertainty. For this reason, each company's specific situation, long-term objectives, and resources must be considered individually when determining whether or not cross-listing is viable. Cross-listing isn't a panacea, but it may help companies reach a wider audience and get access to international financial markets. To assess whether the possible benefits align with the company's overall aims and ability to handle the accompanying complications, the company must balance the benefits against the obstacles and complexity.

Agyemang, A., Balli, F., Gregory-Allen, R. and Balli, H.O., 2023. Cross-listing flows under uncertainty: an international perspective. Applied Economics, pp.1-18.

Alderighi, S., 2020. Cross-listing in the European ETP market. Economics Bulletin, 40(1), pp.35-40.

Areneke, G. and Kimani, D., 2019. Value relevance of multinational directorship and cross-listing on MNEs national governance disclosure practices in Sub-Saharan Africa: Evidence from Nigeria. Journal of World Business, 54(4), pp.285-306.

Bris, A., Cantale, S. and Nishiotis, G.P. (2005). A Breakdown of the Valuation Effects of International Cross-Listing. SSRN Electronic Journal. doi:https://doi.org/10.2139/ssrn.868485.

Chen, C., Shi, S., Song, X. and Zheng, S.X., 2021. Financial constraints and cross-listing. Journal of International Financial Markets, Institutions and Money, 71, p.101290.

Diniz-Maganini, N., Rasheed, A.A., Yaşar, M. and Hua Sheng, H., 2023. Cross-listing and price efficiency: An institutional explanation. Journal of International Business Studies, 54(2), pp.233-257.

Dodd, O. and Gilbert, A., 2016. The impact of cross‐listing on the home market's information environment and stock price efficiency. Financial Review, 51(3), pp.299-328.

Esqueda, O.A., 2017. Controlling shareholders and market timing: Evidence from cross-listing events. International review of financial analysis, 49, pp.12-23.

Filip, A., Huang, Z. and Lui, D., 2020. Cross-listing and corporate malfeasance: Evidence from P-chip firms. Journal of Corporate Finance, 63, p.101232.

Garanina, T. and Aray, Y., 2021. Enhancing CSR disclosure through foreign ownership, foreign board members, and cross-listing: does it work in Russian context?. Emerging Markets Review, 46, p.100754.

Ghosh, C. and He, F., 2017. The diminishing benefits of US cross-listing: Economic consequences of SEC Rule 12h-6. Journal of Financial and Quantitative Analysis, 52(3), pp.1143-1181.

Jackson Jr, R.J. and Taylor, D.J., 2022. Holding foreign insiders accountable. NYU Law and Economics Research Paper, (22-16).

Kamarudin, K.A., Ariff, A.M. and Jaafar, A., 2020. Investor protection, cross-listing and accounting quality. Journal of Contemporary Accounting & Economics, 16(1), p.100179.

Koh, Y. et al. (2013) ‘Determinants of involuntary cross-listing: US restaurant companies’ perspective’, International Journal of Contemporary Hospitality Management, 25(7), pp. 1066–1091. doi:10.1108/ijchm-10-2012-0185.

Lei, Q., Attari, M.U.Q., Hayat, M., Ahmad, M.M., Haseeb, A. and Rafique, A., 2023. Mapping the Themes Underlying the Literature on Cross-Listing of Shares—A Contemporary Corporate Strategy of Sustainable Growth. Sustainability, 15(12), p.9316.

Li, H., 2019. Direct overseas listing versus cross-listing: A multivalued treatment effects analysis of Chinese listed firms. International Review of Financial Analysis, 66, p.101391.

Mrad, M., 2022. Accounting conservatism and corporate cross-listing: The mediating effect of the corporate governance. Cogent Economics & Finance, 10(1), p.2090662.

Reiter, N., 2021. Investor communication and the benefits of cross-listing. Journal of Accounting and Economics, 71(1), p.101356.

Sarkissian, S. and Schill, M.J., 2016. Cross-listing waves. Journal of Financial and Quantitative Analysis, 51(1), pp.259-306.

Shi, H., Zhang, X. and Zhou, J., 2018. Cross-listing and CSR performance: Evidence from AH shares. Frontiers of Business Research in China, 12(1), pp.1-15.

Song, S., Zeng, Y. and Zhou, B., 2021. Information asymmetry, cross-listing, and post-M&A performance. Journal of Business Research, 122, pp.447-457.

Statista.com (2023) NYSE and NASDAQ: Market cap comparison 2023, Statista. Available at: https://www.statista.com/statistics/1277195/nyse-nasdaq-comparison-market-capitalization-listed-companies/ (Accessed: 10 October 2023).

Statista Research Department and 22, M. (2023) NYSE and NASDAQ: Listed companies comparison Q1 2023, Statista. Available at: https://www.statista.com/statistics/1277216/nyse-nasdaq-comparison-number-listed-companies/ (Accessed: 10 October 2023).

Sec.gov (2022) Form 144-resources for filing electronically, SEC Emblem. Available at: https://www.sec.gov/edgar/filer-information/form-144-resources-filing-electronically (Accessed: 10 October 2023).

Temouri, Y., Driffield, N. and Bhaumik, S.K., 2016. A strategic perspective of cross-listing by emerging market firms: Evidence from Indonesia, Mexico, Poland and South Africa. Journal of International Management, 22(3), pp.265-279.

Tripathy, N., 2020. Does Cross-Listing Create Value for Firms. The Empirical Economics Letters, 19(8), pp.823-835.

Wang, S. and Wu, S., 2019. Compliance costs and comparability benefits of cross-listing: Evidence from accounting standard differences and IFRS adoption. Asian review of accounting, 27(4), pp.563-594.

Xu, H., Fu, Y. and Jasinskas, E., 2021. Can cross-listing improve investment efficiency? Empirical evidence from China. Economic research-Ekonomska istraživanja, 34(1), pp.1789-1813.

Essay: 10 Pages, Deadline: 2 days

They delivered my assignment early. They also respond promptly. This is excellent. Tutors answer my questions professionally and courteously. Good job. Thanks!

![]() User ID: 9***95 United

States

User ID: 9***95 United

States

Report: 10 Pages, Deadline: 4 days

After sleeping for only a few hours a day for the entire week, I was very weary and lacked the motivation to write anything or think about any suggestions for the writer to include in the paper. I am glad I chose your service and was pleasantly pleased by the quality. The paper is complete and ready for submission to the professor. Thanks!

![]() User ID: 9***85 United

States

User ID: 9***85 United

States

Assignment: 8 Pages, Deadline: 3 days

I resorted to the MBA assignment Expert in the hopes that they would provide different outcomes after receiving unsatisfactory results from other assignment writing organizations, and they genuinely are fantastic! I received exactly what I was looking for from this writing service. I'm grateful.

![]() User ID: 9***55

User ID: 9***55

Assignment: 13 Pages, Deadline: 3 days

Incredible response! I could not believe I had received the completed assignment so far ahead of the deadline. Their expert team of writers effortlessly provided me with high-quality content. I only received an A because of their assistance. Thank you very much!

![]() User ID: 6***15 United

States

User ID: 6***15 United

States

Essay: 8 Pages, Deadline: 3 days

This expert work was very nice and clean.expert did the included more words which was very kind of them.Thank you for the service.

![]() User

ID: 9***95 United

States

User

ID: 9***95 United

States

Report: 15 Pages, Deadline: 5 days

Cheers on the excellent work, which involved asking questions to clarify anything they were unclear about and ensuring that any necessary adjustments were made promptly.

![]() User ID: 9***95 United

States

User ID: 9***95 United

States

Essay: 9 Pages, Deadline: 5 days

To be really honest, I can't bear writing essays or coursework. I'm fortunate to work with a writer who has always produced flawless work. What a wonderful and accessible service. Satisfied!

![]() User ID: 9***95

User ID: 9***95

Essay: 12 Pages, Deadline: 4 days

My essay submission to the university has never been so simple. As soon as I discovered this assignment helpline, however, everything improved. They offer assistance with all forms of academic assignments. The finest aspect is that there is also an option for escalation. We will get a solution on time.

![]() User ID: 9***95 United

States

User ID: 9***95 United

States

Essay: 15 Pages, Deadline: 3 days

This is my first experience with expert MBA assignment expert. They provide me with excellent service and complete my project within 48 hours before the deadline; I will attempt them again in the future.

![]() User ID: 9***95 United

States

User ID: 9***95 United

States