CLWM4100 Taxation Law Case Study 3

Your task is to analyse client information outlined in the three different case studies below and present the findings in three Statement of Advice (approximately 2,000 words).

You are required to prepare Smart Solutions Pty Ltd’s taxation return.

1) You are required to provide advice and tax calculations to Julia and John (directors of Smart Solutions Pty Ltd) regarding the tax payable by the company.

2) You are required to calculate the capital gains tax for Julia and Smart Solutions Pty Ltd.

3) You are required to complete the franking account and tax implications on dividend received by Smart Solutions Pty Ltd shareholders.

For each question you are expected to:

1) identify the facts and issues for each case

2) apply the relevant legislation and/or case law.

Statement of Advice 1 – Prepare a tax return for an entity (Australian private company) (10 marks for technical and calculation accuracy and relevance and 10 marks for writing style; refer to marking rubric for more guidance.)

In your current role, you are responsible for providing taxation services to individual/business clients. You conducted an initial meeting with two (2) clients (Julia and John Smart, both Australian residents) to obtain and document all the relevant information which is required to prepare the relevant tax documentation. Both Julia and John are directors of Smart Solutions Pty Ltd, an Australian resident private company with a corporate tax rate for imputation purposes of 30% for the 2021/22 income year. The clients have requested that you evaluate their tax position and provide recommendations relating to income tax liability and the optimum tax treatment. Smart Solutions Pty Ltd sells coffee machines using accrual basis accounting for tax purposes.

Receipts and payment details as at 30 June 2022 are as follows (ignore GST and small business concessions).

Cash received for Sales (note 1) $278,000

Dividend received (note 2) $8,720

Purchases of inventory (note 3) $97,000

Net wages paid to employees $57,890

PAYG withholding paid to the ATO $12,780

Superannuation paid (note 4) $4,987

PAYG instalment paid the ATO (note 5) $5,210

Fringe benefit tax paid to the ATO $11,210

Income tax refund (note 6) $30,000

Purchase of motor vehicle (note 7) $52,000

Other deductible expenses $26,900

Notes

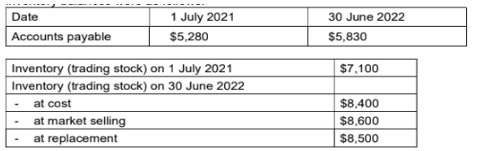

Note 1) All sales during 2022 income year were on credit. Account receivable balances were as follows.

Note 2) Dividend income received by Smart Solutions Pty Ltd for the year included:

• On 30/8/2021, a dividend of $3,600 received from Australian Bank Ltd (an Australian resident public company for tax purposes) franked to 60%.

• On 28/2/2022, an unfranked dividend of $5,120 from Lowest Ltd (an Australian resident public company for tax purposes).

Note 3) All inventory purchases during 2022 tax year were on credit. Account payable and inventory balances were as follows.

Note 4) As per the ledger balances on 30 June 2022, Superannuation payable for June quarter was amounted to $1,727. The payment is due by 28 July 2022.

Note 5) As per the ledger balances on 30 June 2022, PAYG instalment liabilities payment and payable information are as follows.

24/8/2021 PAYG instalment paid for June quarter 2021 $ 860

25/11/2021 PAYG instalment paid for September quarter 2021 $1,450

28/2/2022 PAYG instalment paid for December quarter 2021 $1,450

26/5/2022 PAYG instalment paid for March quarter 2022 $1,450

June quarter 2022 was amounted to $1,450. The payment will be paid on 25 August 2022.

Note 6) The tax refund was paid on 25 February 2022.

Note 7) The motor vehicle (Toyota Hatchback) was used to deliver coffee machines. Both directors wish to use the taxation effective life to depreciate the machine.

1) John wishes to minimise the income tax for 2021/22. Calculate Smart Solutions Pty Ltd’s net tax liability in respect of the income that it derived in the tax year 2021/22.

2) Advise assessability of receipts and deductibility of payments with explanations (Sales, Dividend income, Trading Stock, PAYG withholding, PAYG instalment, Superannuation guarantee, fringe benefits, Dividend paid and motor vehicle purchase). Include section numbers and/or cases in your explanations.

Statement of Advice 2 – Advice on company franking account and distributions (10 marks for technical and calculation accuracy; refer to marking rubric for more guidance)

Julia and John seeking your advice regarding Smart Solutions Pty Ltd’s franking account. (Please note: use all figures/information provided from Statement of Advice 1 above to construct the franking account for 2021/22. Opening balance is provided below).

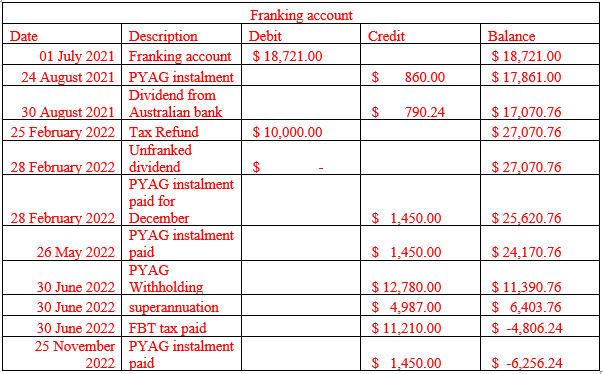

1) 1 July 2021, the balance in Smart Solutions Pty Ltd’s franking account was $18,721. Construct Smart Solutions Pty Ltd’s franking account for the 2021/22 financial year. You also need to calculate the franking account balance as at 30 June 2022.

2) Smart Solutions Pty Ltd wishes to pay a final fully franked dividend of $40,000 on 30 June 2022. However, Julia and John are concerned about the franking account to go into deficit.

Calculate and advise the maximum frankable distribution amounts that Smart Solutions Pty

Ltd can pay as fully franked dividend. What are the tax consequences if Smart Solutions Pty

Ltd goes ahead and pays $40,000 fully franked dividend on 30 June 2022?

3) Assuming Smart Solutions Pty Ltd paid $40,000 fully franked dividend on 30 June 2022 (only dividend paid for the year), comment on the tax treatment of the dividend to the following four

(4) shareholders:

• Julia and John Smart receive a dividend of $15,000 each. They are Australian residents at the highest marginal tax rate.

• $5,000 to Justin Smart, the son of Julia and John, who has been studying in London for three years and is a foreign resident.

• $5,000 to Leaf Pty Ltd, an Australian private company with a 30% company income tax rate.

Advise how each of the above four shareholders of Smart Solutions Pty Ltd would be taxed on the distribution received in 2021/22.

To calculate the tax liability for the smart solution PTY Limited, the income tax assessment Act 1997, and the relevant taxation ruling as suggested by ATO are required to be evaluated.

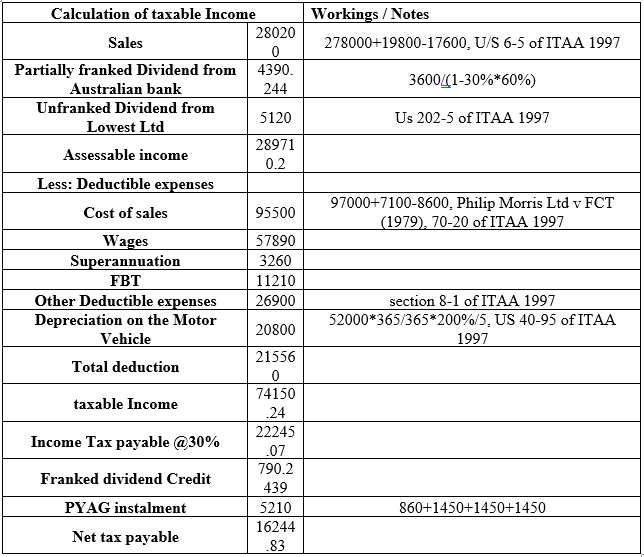

Based on the calculation, it is identified that the total tax liability for the financial year 2021/22 for the organisation is $22185.07. According to the MBA Assignment Expert overview, When the applicable corporate tax is 30%, and the company is not a small business entity, they are not eligible to get the small business concessional tax rate. In terms of PYAG, the company has already made a payment of taxes 5210 during the financial year. Therefore, the company’s net tax liability is $16184.83.

Here, to minimise the tax liability, one available strategy is to maximise the claimable depreciation on the motor vehicle in accordance with division 40 of the Income Tax Assessment Act 1997. The process of doing so is by making a judgement where the life of the Asset should be minimised to maximise the claim, and here, the diminishing value method should be used for getting the maximum depreciation allowance for the taxation purpose.

Additionally, there is an opportunity for deciding the valuation of the trading stock in accordance with section 70-45 of ITAA 1997, where the taxpayer has the preference for selecting the valuation method for the inventory. The only restriction is that the valuation which is used for the current year closing should be equivalent to the next year opening balance for the trading stock. Hence to minimise the tax liability, the market selling price for the trading stock is selected, which is valuing the trading stock on the closing date at $8600.

The accessibility of receive the deductibility for the payments for the smart solution Pty Limited is as follows:

Sales

In the given case scenario, the company can recognise the sales for the period for the tax assessment purpose for which the total collection is not relevant; however, the total sales made by the company in accordance with the accrual system should be followed. In accordance with the calculation, it is clearly identified that the company is required to report the total sales value of $280200 for the tax assessment purpose in accordance with section 6.5 of the income tax assessment Act 1997 (Fullarton and Pinto, 2020).

Dividend Income

The dividend income for the corporate entity will be considered separately in accordance with Section 44 of ITAA 1997, as per which the dividend income received by the company will be considered as ordinary income at the same time. In accordance with SE 207-20 of ITAA 1997, Smart home is required to use the gross-up approach for identifying the total value of dividend received at the same time the company is eligible to get a deduction for the Franked amount which is already paid at the time of receiving the dividend. Therefore, the dividend received from the Australian bank is required to be grossed up, which indicates a total dividend income of $4390.24.

However, the dividend received from the lowest Limited is unfranked there, for the entire dividend should be considered without adjustment.

Trading stock

In accordance with section 70-45 of ITAA 1997, the taxpayer can determine the value of the trading stock at the end of the year. As the taxpayer has the opportunity for the selection of the valuation method for the trading stock, the maximum value out of the three options is selected for maximising the cost of sales for minimising the tax liability.

PYAG withholding

The PYAG withholding account for the taxes that the company has charged from the employees and pays to the Australian taxation office, and it is not an expense for the business. Rather it is a service that the company is charging the taxes and making payment for them on behalf of the employees.

PYAG instalment

The PYAG Instalment is the process where the companies are required to make a partial payment for their estimated tax liability on a timely basis, mostly on a quarterly basis, as a part of the tax repayment. The balance for the Tax amount due at the end of the tax period will be adjusted with the total tax liability to calculate the net taxes paid or refund available for the business. However, it is not an expense for the taxation purpose there, so it cannot be deducted.

Superannuation

The superannuation expenses for the business will be considered as a part of the various expenses there, for the taxpayer will get a deduction for the same in accordance with section 8-1 of ITAA 1997

Fringe benefit:

In accordance with the fringe benefits tax assessment Act 1986 under Section 136(1), The taxpayer is required to make the payment for the taxes on the benefit provided by the company to the employee or any associate of the employed during employment. This will be considered as an expense for the taxation purpose there, for the entire amount of fringe benefit taxes paid by Smart Solution can be considered as a deduction in accordance with section 8-1 of ITAA 1997.

Dividend paid

The dividend payment made by the company will not be considered as an expense for taxation purpose Because this is not a business expense for generating the accessible income for the business. However, at the time of making the dividend payment, the company will be required to charge the franking at the imputation rate of 30% (O’Connell, 2021).

Motor Vehicle Purchase

To get the depreciation for the motor vehicle, there are two different options which can be used for the calculation of the depreciation method is that the prime cost method and the diminishing value method. However, the depreciation that can be charged using the diminishing value method is higher than the total depreciation that can be charged using the prime cost method. As the tax has the Liberty to select that method, which is applicable to the organisations, the diminishing value method is selected for minimising the tax liability. In accordance with section 40-95, the taxpayer can make a Reliable estimation for the life of the asset as per which It is assumed that the life of the motor vehicle will be 5 years and the depreciation of $20800Is charged to the account.

Other deductible expenses

The other deductible expenses for the business are identified at $26900, which is considered as the allowable deduction in accordance with section 8-1 of ITAA 1997.

In accordance with section 202-10 of ITAA 1997, The franking account represents an income tax account in which the income taxes already paid by the company on the prophets for the distributions made and the taxes paid by the company are adjusted. This particular account will have debit and credit Adjustments, which are done as follows:

Franking credit adjustment (Section 205-15 of ITAA 1997)

In accordance with the section, the franking credit adjustments will be made on the following events:

● The company makes the payment for the PYAG (Brown et al., 2020)

● The organisation receives franked distribution directly or indirectly.

● The organisation incurs liability to pay franking deficit.

Franking debit adjustment (section 205-30 of ITAA 1997)

In accordance with the section 205-30 of the say that the franking credit account will have a debit adjustment for the following circumstances

● The company makes franked distribution.

● The company received any income tax refund.

● The company violates the franking rules (Australian Taxation Office, 2016)

In the given case scenario, if the company is within to make distribution for $40000, then in such case, they will be required to make a payment for the franking amount of $13743.76 on the distributed dividend in access. However, the current balance for the franking account is -$6256.24, whereas the additional tax liability for the Franked amount of the dividend payable is $12000 ($40000*30%) (assuming 100% franked distribution). As the amount on the closing balance of the franking account at the end of the period is already in deficit making additional distribution of dividend will critically impact the franking account which will initiate additional franking deficit of $12000, or the net franking deficit or the Debit balance will be $-18256.24.

In accordance with the franking deficit tax, 204-45(2) of the income tax assessment Act 1997 a company will be required to pay that access if they are having a debit franking balance account which will incur liability for the payment of deficit amount. However, it should not be considered as a penalty unless it is exceeding the 10% of the total amount of ranking credit arising during the income year as suggested by section 205-70(2) of ITAA 1997.

Therefore, if the company decides to make payment for the dividend, it will get impacted because of the dividend payment, and neither will it face franking deficit-related issues. Hence If the company is filling to make additional payment for the dividend then it will be required to make additional payment in order to make the franking account by at least the amount of deficit.

Julia and John receive a dividend of $15000 each:

In accordance with the provisions of the act Under section 207-20 of ITAA 1997, the taxpayer pair will be required to grow up the dividend received with the Franked amount in case of resident individual. Julia and John Smart is considered to be Australian resident for taxation purpose there for the amount they are getting as a dividend from Smart Pty will be considered as a dividend income attached to the Franked proportion, that the company has paid taxes on the dividend at 30%. However, as the individual is having or making text payments at the highest marginal taxes, which is 45%, the tax liability for the individual will increase. In that case, the tax liability which John and Julia are required to pay individually on the dividend in compressive from Smart Home will be $9642.6 each ($21428.57*45) % (Refer to appendix b)

At the same time, in accordance with section 202-5 of ITAA 1997, the tax pair can get the direction for the franking credit attached to the dividend payment, which is here $6428.57. Therefore, the additional tax liability borne by the taxpayers will be $3214.29 each.

$5000 Received by Justin Smart:

In the given case scenario, the dividend received by Justin Smart will be considered as income generated in Australia; therefore, it will be taxed accordingly as the entire dividend will be received as ordinary income and will be taxed in accordance with sections 6-5 of ITAA 1997.

However, as specified under section 207.70 of ITAA 1997, the gross of and the tax offset do not apply for the non-resident entities with there is a corporate entity or the individual 4 The franking credit will not be available for Justin. But Justin will be required to make payment for the taxes for the dividend it is receiving from the Australian territory.

$5000 Received by the Australian private company

If the Australian private company is receiving the fully Franked dividend paid by the smart solutions, no additional adjustments will be required for the same because the Australian private company, Leaf Pty is in the same income tax rate of 30% at which the smart solution Pty has paid the dividend. The Adjustment in the franking account will be made in accordance with the respective provisions.

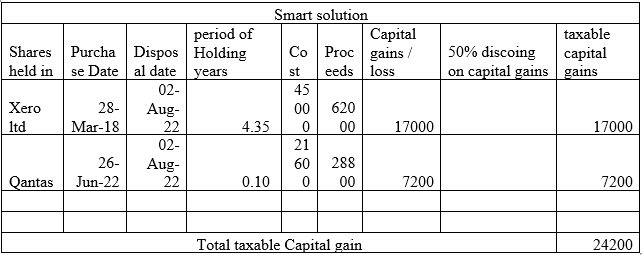

Statement of Advice 3 – Advice on net capital gains

In the given case scenario, the shares getting sold by the entities are considering the capital gains taxes in accordance with the subdivision 104-A of ITAA 1997 in the way of disposal of Capital Asset.

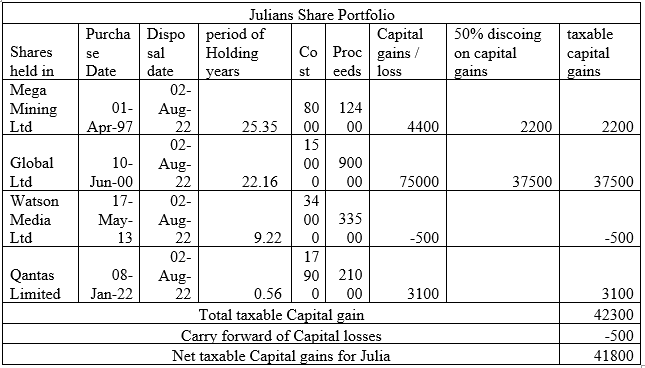

Based on the information provided, the capital gains made by Julia’s Sheer portfolio have some capital gains and capital loss adjustments; however, to minimise the tax liability, the tax pair is entitled to get a 50% discount on the capital gains if the period of holding for the Capital Asset is more than one year. Therefore, Julia is eligible to get a 50% deduction for the sale of Mega Mining Limited and the Global Limited shares (US 115-5 of ITAA 1997) (Income tax assessment act 1997)

Additionally, the carry forward of the capital losses for the previous financial year Is eligible to get adjusted into the current financial year capital gains in accordance with section 102-10(2) of ITAA 1997 (Maconi, 2020).

Therefore, the taxable capital gains of Julia will be $41800 after getting all the eligibility deductions.

For the corporate entity, the entire amount of difference between the capital proceeds received and the cost base will be considered for the capital gains purpose how. Were the 50% discount option will not be available for the corporate entities. Therefore, the smart solution is required to include the taxable capital gain of $24200 for their tax calculation.

Australian Taxation Office (2016) Franking account, Australian Taxation Office. Available at: https://www.ato.gov.au/Business/Imputation/Paying-dividends-and-other-distributions/Franking-account/

Brown, R., Lim, Y., Evans, C., Cassidy, J., Cheng, M.H.A., Le, T., Huang, E., Oguttu, A.W., Kayis-Kumar, A., Smith, A. and Plekhanova, V., eJournal of Tax Research. https://www.unsw.edu.au/content/dam/pdfs/unsw-adobe-websites/business-school/faculty/our-research/past-issues/bus-2020/2020-volume-18-number-2/BUS-2020-V18-paper6-v18-n2.pdf

Fullarton, L. and Pinto, D., 2020. The Wade Case: An Analysis. This article was first published by Thomson Reuters New Zealand in the New Zealand Journal of Taxation Law and Policy and should be cited as Alexander Fullarton and Dale Pinto, The Wade Case: an analysis,(2021), 27(2). https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3546731

Income tax assessment act 1997 - sect 115.10 Who can make a discount capital gain? Available at: http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s115.10.html

Marconi, F., 2020. Amendments to the small business capital gains concessions. QUEENSLAND LAWYER, 38(3), pp.192-198. https://maconibarrister.com/wp-content/uploads/2020/02/fmaconi_ql_v38_pt3.pdf

O’Connell, A., 2021. Is it really a charity? Membership-based entities as charities: The Australian experience. In The Routledge Handbook of Taxation and Philanthropy (pp. 115-137). Routledge. https://library.oapen.org/bitstream/handle/20.500.12657/52010/1/9781000514216.pdf#page=136

Essay: 10 Pages, Deadline: 2 days

They delivered my assignment early. They also respond promptly. This is excellent. Tutors answer my questions professionally and courteously. Good job. Thanks!

![]() User ID: 9***95 United

States

User ID: 9***95 United

States

Report: 10 Pages, Deadline: 4 days

After sleeping for only a few hours a day for the entire week, I was very weary and lacked the motivation to write anything or think about any suggestions for the writer to include in the paper. I am glad I chose your service and was pleasantly pleased by the quality. The paper is complete and ready for submission to the professor. Thanks!

![]() User ID: 9***85 United

States

User ID: 9***85 United

States

Assignment: 8 Pages, Deadline: 3 days

I resorted to the MBA assignment Expert in the hopes that they would provide different outcomes after receiving unsatisfactory results from other assignment writing organizations, and they genuinely are fantastic! I received exactly what I was looking for from this writing service. I'm grateful.

![]() User ID: 9***55

User ID: 9***55

Assignment: 13 Pages, Deadline: 3 days

Incredible response! I could not believe I had received the completed assignment so far ahead of the deadline. Their expert team of writers effortlessly provided me with high-quality content. I only received an A because of their assistance. Thank you very much!

![]() User ID: 6***15 United

States

User ID: 6***15 United

States

Essay: 8 Pages, Deadline: 3 days

This expert work was very nice and clean.expert did the included more words which was very kind of them.Thank you for the service.

![]() User

ID: 9***95 United

States

User

ID: 9***95 United

States

Report: 15 Pages, Deadline: 5 days

Cheers on the excellent work, which involved asking questions to clarify anything they were unclear about and ensuring that any necessary adjustments were made promptly.

![]() User ID: 9***95 United

States

User ID: 9***95 United

States

Essay: 9 Pages, Deadline: 5 days

To be really honest, I can't bear writing essays or coursework. I'm fortunate to work with a writer who has always produced flawless work. What a wonderful and accessible service. Satisfied!

![]() User ID: 9***95

User ID: 9***95

Essay: 12 Pages, Deadline: 4 days

My essay submission to the university has never been so simple. As soon as I discovered this assignment helpline, however, everything improved. They offer assistance with all forms of academic assignments. The finest aspect is that there is also an option for escalation. We will get a solution on time.

![]() User ID: 9***95 United

States

User ID: 9***95 United

States

Essay: 15 Pages, Deadline: 3 days

This is my first experience with expert MBA assignment expert. They provide me with excellent service and complete my project within 48 hours before the deadline; I will attempt them again in the future.

![]() User ID: 9***95 United

States

User ID: 9***95 United

States