BUS9004 Accounting & Finance Report 2

You are considering taking up a position as assistant to the financial controller of one of two companies. You have been interviewed by each company and you expect to be offered the position by both companies. You are not sure which company you want to work for, so you decide to analyse the latest financial statements of each company to help you make the decision. You want to work for the company that is the most profitable and is financially secure in both the short-term and the longer term.

Each student will be provided with the current year financial statements of 2 companies.

1. Using Excel, calculate a selection of financial ratios and conduct analysis on each company. Be sure to use formulas wherever possible.

2. Explain what each key ratio and the analysis indicates, individually and in aggregate.

3. What company have you chosen to work for? Explain what persuaded you to choose that company? In your answer comment on the information, you generated on the profitability, efficiency and liquidity of each company.

4. What additional information would you like to have about each company to help you make your decision?

In this assessment, you are considering taking up a position as assistant to the financial controller of one of two companies. You have been interviewed by each company and you expect to be offered the position by both companies. You are not sure which company you want to work for, so you decide to analyze the latest financial statements of each company to help you make the decision. You want to work for the company that is the most profitable and is financially secure in both the short-term and the longer term.

Each student will be provided with the current year financial statements of 2 companies.

Your report should consist of the following key components of a report:

1. Executive Summary (not included in your word count)

2. Introduction

3. Main Body

4. Conclusion

5. References (not included in your word count)

Introduction: (approximately 200 words)

Provide an overview of what your report is about and what the reader can expect to see in the remainder of the report.

Main Body: (approximately 1,500 words)

You should address the following questions in the main body of your report.

1. Using Excel, calculate a selection of financial ratios and conduct analysis on each company. Be sure to use formulas wherever possible.

2. Explain what each key ratio and the analysis indicates, individually and in aggregate.

3. What company have you chosen to work for? Explain what persuaded you to choose that company? In your answer comment on the information, you generated on the profitability, efficiency and liquidity of each company.

4. What additional information would you like to have about each company to help you make your decision?

Conclusion:

Provide a 1 paragraph summary of the results from your report (approximately 200 words).

References:

Minimum of 5 references.

This analysis compares ANZ Bank and Commonwealth Bank's latest financial statements to determine who has superior profitability and financial stability. Thus, before hiring, one must assess the company's finances and performance.

The paper will address three categories of key financial ratios to accomplish so: Direct profit: ROE, ROA, and Net Profit Margin; solvability: Current and Quick Ratios; productive: Asset and Receivable Turnover Ratios. These ratios will show each company's ability to make profits, meet short-term obligations, and manage resources efficiently.

Melbourne-based ANZ Bank is a significant Australian bank. It offers several financial services and has branches worldwide. Commonwealth Bank, another Australian banking and financial services giant, operates in Sydney and provides banking, insurance, investing, and wealth management. They're both from the financial field, so you should investigate their finances to see whether you want to work for them for MBA assignment expert .

2.1 Financial Ratios Calculation and Analysis

Profitability Ratios

.png)

Table 1: PROFITABILITY RATIOS

(Source: Excel)

Return on Equity (ROE): ROE is the assessment of a company’s ability to generate profit from its shareholders’ funds.

It is calculated as: ROE=" Net Income " /" Total Equity "

For ANZ Bank: ROE=7,098/70,046=0.101 or 10.1%

For Commonwealth Bank: ROE=10,188/72,005=0.141 or 14.1%

Return on Assets (ROA): As a measure of performance, R OA show how effectively the business is using asset to generate returns. It is calculated as: ROA=" Net Income " /" Total Assets "

For ANZ Bank: ROA=7,098/1,105,620=0.0064 or 0.64%

For Commonwealth Bank: ROA=10,188/1,252,845=0.0081 or 0.81%

Net Profit Margin: Another ratio used in the analysis of profitability is the net income to total sales ratio that shows how much net income is made for every dollar of sales. It is calculated as: Net Profit Margin =" Net Income " /" Sales "

For ANZ Bank: Net Profit Margin =7,098/96,773=0.073 or 7.3%

For Commonwealth Bank: Net Profit Margin =10,188/81,462=0.125 or 12.5%

Return on Assets (ROA)

ROA=" Net Income " /" Total Assets " ×100

For ANZ: 0.64%

For Commonwealth Bank: 0.81%

.png)

Table 2: LIQUIDITY RATIOS

(Source: Excel)

Current Ratio: The current ratio aims at determining a company’s capability to meet its current obligations using the current assets. It is calculated as: Current Ratio =" Current Assets " /" Current Liabilities "

For ANZ Bank: Current Ratio =14,583/102,481=0.14

For Commonwealth Bank: Current Ratio =40,917/26,709=1.53

Quick Ratio (Acid Test Ratio): It provides information on the firm’s short term liquidity position without considering inventory in its calculations. It is calculated as: Quick Ratio =

Current Assets-Inventories

Current Liabilities

For ANZ Bank: Quick Ratio =(14,583-13,626)/102,481=0.01

For Commonwealth Bank: Quick Ratio =(40,917-12,839)/26,709=1.05

Cash Ratio: The cash ratio calculates the extent to which a company can meet short-term obligations using cash and Cash equivalents. It is calculated as: Cash Ratio =" Cash " /" Current Liabilities "

For ANZ Bank: Cash Ratio =145,647/102,481=1.42

For Commonwealth Bank: Cash Ratio =107,172/26,709=4.01

Operating Cash Flow Ratio

Operating Cash Flow Ratio =" Operating Cash Flow " /" Current Liabilities "

For ANZ: 0.08

For Commonwealth Bank: 0.31

.png)

Table 3: Efficiency Ratios

(Source: Excel)

Asset Turnover Ratio: This ratio compares the total assets of a business to its total sales and it shows to what extent a business is utilizing its assets to generate sales. It is calculated as: Asset Turnover Ratio =" Net Sales " /" Total Assets "

For ANZ Bank: Asset Turnover Ratio =96,773/1,105,620=0.087 or 0.09

For Commonwealth Bank: Asset Turnover Ratio =81,462/1,252,845=0.065 or 0.07

Receivables Turnover Ratio: This ratio tells the extent to which a company is capable of collecting its receivables. It is calculated as: Receivables Turnover Ratio =" Net Sales " /" Accounts Receivables "

For ANZ Bank: Receivables Turnover Ratio =96,773/3,508=27.6

For Commonwealth Bank: Receivables Turnover Ratio =81,462/2,952=27.6

Accounts Payable Days: This ratio establishes the average time taken by a company to clear its dues to its suppliers. It is calculated as: Accounts Payable Days =" Account Payables " /" Purchases " ×360

For ANZ Bank: Accounts Payable Days =14,431/74,446×360=69.8 days

For Commonwealth Bank: Accounts Payable Days =15,255/57,066×360=96.2 days

Inventory Turnover Ratio

Inventory Turnover Ratio =" COGS " /" Inventory "

For ANZ: 5.46

For Commonwealth Bank: 4.44

.png)

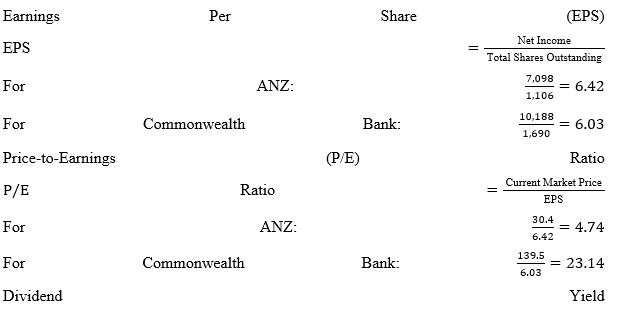

Table 4: Investment ratios

(Source: Excel)

.png)

Table 5: Gearing ratio

(Source: Excel)

Debt-to-Equity Ratio

Debt-to-Equity Ratio =" Total Debt " /" Total Equity "

For ANZ: 241,687/70,046=3.45

For Commonwealth Bank: 267,555/72,005=3.72

Equity Multiplier

Equity Multiplier =" Total Assets " /" Total Equity "

For ANZ: 1,105,620/70,046=15.78

For Commonwealth Bank: 1,252,845/72,005=17.40

Interest Coverage Ratio

Interest Coverage Ratio =" EBIT " /" Interest Expense "

For ANZ: 10,023/33,321=0.30

For Commonwealth Bank: 14,455/21,419=0.67

Debt Ratio

Debt Ratio =" Total Debt " /" Total Assets "

For ANZ: 241,687/1,105,620=0.22

For Commonwealth Bank: 267,555/1,252,845=0.21

Profitability Comparison: With regards to the profitability, Commonwealth Bank has better numbers than ANZ Bank with higher ROE of (14.1% vs 10.1%), ROA of (0.81% vs 0.64%,) and net profit margin of (12.5% vs 7.3%). This means that out of the three, Commonwealth Bank has a better capacity of generating profit per dollar of equity, asset and sales.

Liquidity Comparison: Commonwealth Bank has a better liquidity position with a higher Current Ratio (1.53 vs. 0.14), Quick Ratio (1.05 vs. 0.01), and Cash Ratio (4.01 vs. 1.42). This implies that the CCM has more ability in fulfilling its near-term obligations and has a better cash flow position than that of ANZ Bank.

Efficiency Comparison: Both banks have similar Receivables Turnover Ratios (27.6), but Commonwealth Bank has a slightly lower Asset Turnover Ratio (0.07 vs. 0.09). As with respect to efficiency in generating sales, ANZ Bank proves to be more efficient in using its assets.

Profitability Ratios

Return on Equity (ROE): ROE measures how effectively a company generates profit relative to shareholders' equity. Commonwealth Bank's ROE stands at 14.1%, compared to ANZ Bank's 10.1%. Commonwealth Bank with a higher ROE is efficiently using the equity capital to generate better profits for its shareholders. On the other hand, the lower ROE can be attributed to ANZ Bank being less efficient in turning equity into net income, which may suggest a poorer performance on profitability (Wsj, 2024).

Return on Assets (ROA): ROA assesses how well a company uses its assets to generate profit. Commonwealth Bank has an ROA of 0.81%, while ANZ Bank's ROA is 0.64%. This means that compared to the industry average, Commonwealth Bank better manages its asset base to generate net income, as seen by the higher ROA (Mann et al. 2024). A lower ROA as compared to Her personalization means that ANZ Bank could be less efficient in utilising its assets in making profits which could affect its profitability levels.

Net Profit Margin: The Net Profit Margin demonstrates how many coins of the realm or units of sales translates into Net Profit. From the prepared and analyzed financial statements, it is evident that Commonwealth Bank’s margin is 12.5%, while ANZ Bank New Zealand has a net interest margin of 7.3%. A higher margin for Commonwealth Bank shows that it keeps a tighter control over it costs and expenses as compared to its sales which mean it is efficient.

Liquidity Ratios

Current Ratio: The Current Ratio indicates the capacity of a company in the payment of near-term financial obligations using near term resources. With regards to its total assets, Commonwealth Bank’s hedging ratio is 1.53 it is clear that the organisation has more than adequate current assets to cover current liabilities, which shows good short- term solvency. Conversely, at the time of consolidation, the ratio of INT, NCC and O/I in the current period at ANZ Bank was 0. After analyzing FL’s ratios: 14, it raises concerns regarding the company’s inability to meet its current liabilities through current assets, thereby suggesting that FL might be facing liquidity problems.

Quick Ratio: The Quick Ratio measures a company’s capacity to satisfy current liabilities without turning to stock (Olayinka, 2022). The quick ratio of the Commonwealth Bank is 1. In the line 05 we can get the impression that it has enough cash and cash equivalents to cover all its current liabilities. This is so because since ANZ Bank’s Quick Ratio is 0. 01 is, however, very low which shows a very severe liquidity problem since it cannot afford to cover most of its current obligations without converting inventory into cash.

Efficiency Ratios

Asset Turnover Ratio: This ratio measures how effectively a company uses its assets to generate sales. ANZ Bank’s Asset Turnover Ratio of 0.09 is slightly higher than Commonwealth Bank's 0.07, suggesting ANZ Bank is marginally more efficient in utilizing its assets to generate sales.

Receivables Turnover Ratio: The Receivables Turnover Ratio shows how efficiently a company collects receivables. Both ANZ Bank and Commonwealth Bank have identical Receivables Turnover Ratios of 27.6, indicating similar efficiency in collecting receivables. These observations imply that both firms are good in their management of receivables, thus a boost to their collection of cash in their respective organizations (Lee et al. 2021).

Chosen Company: Based on the financial analysis, I would choose to work for Commonwealth Bank.

Justification:

Profitability: Commonwealth Bank demonstrates superior profitability metrics compared to ANZ Bank. With a Return on Equity (ROE) of 14.1% versus ANZ Bank's 10.1%, Commonwealth Bank provides better returns on shareholders' equity, indicating stronger profitability. Additionally, its Return on Assets (ROA) of 0.81% is higher than ANZ Bank’s 0.64%, reflecting more efficient asset utilization to generate profits. The Net Profit Margin of 12.5% for Commonwealth Bank further underscores its ability to control costs and convert sales into profit more effectively than ANZ Bank, which has a margin of 7.3%.

Efficiency: Otherwise known as Total Asset Returns, ANZ Bank’s Asset Turnover Ratio stands at 0.09 is slightly higher than the Commonwealth Bank at 0.07, even though it is slightly superior, indicating slightly better asset turnover. However, the difference is small and cannot fundamentally offset the other financial advantages. Both companies have a Receivables Turnover Ratio of 27.6, meaning that receivables were also handled at a similar level of effectiveness as inventory.

Liquidity: As to the liquidity ratio analysis, it positively indicates that the Commonwealth Bank has an edge over its competitors. In the same perspective, its current ratio was at 1.53 and the Quick Ratio of 1.05 values shows that this company has strong capacity to support its short-term liabilities by adequate amounts of liquid assets. On the same note, ANZ Bank’s Current Ratio stands at 0.14 and Quick Ratio of 0.01 indicate very poor liquidity positions suggesting the firms are facing real problems in meeting short-term liabilities (Lim and Kumar, 2024).

Desired Information:

To draw a line in between ANZ Bank and Commonwealth Bank more information is needed regarding the financial and operations update.

Non-Operating Income Breakdown:

Knowledge about operating income segmentation is useful to measure the stability of profitability (Hamadneh et al. 2021). This may indicate that Commonwealth Bank’s core operations might not be as good because Net Income often contains non-operating gains from investments or sale of assets. Such specifics would help to clear up whether sales and, consequently, revenues and profits are generated from the business’s main activities or from occasional incidents.

Future Growth Projections:

It is helpful for determining long term growth to understand the company’s future possible growth expectations and requirements. Details on forecasted revenues, market growth, and plans and programmes will help to determine whether each firm has the potential to maintain and increase profitability (Schroeder, Clark and Cathey, 2022). For example, additional information on CBA’s strategy in digital banking or in international markets can provide more evidence for its sound financial status.

Industry-Specific Challenges:

It would be helpful to gain some insight on how each company of this industry is having to deal with, regarding the challenges highlighted above. For instance, information on how ANZ Bank and the Commonwealth Bank respond to regulatory changes, developments in technology or change in the economy, could reveal how they are placed if dealing with risks (Ahmadullo o’g’li, 2023). Details of investment made in technology or changes within the banking regulatory environment would show the respective positioning and sensitivity of the companies within the industry.

Detailed Risk Management:

Details on expenditure on risk management, effectiveness of controls and project risks in terms of market risks, credit risks, and operational risks would enable assessment of how each company coped with uncertainty. More comprehensive reports on all risks and the outlined risk management plans would give a better revelation of their sound financial status and overall business resilience (Haralayya, 2021).

When analyzing cash flow, companies typically employ either the direct or indirect method. Both methods aim to provide insights into how cash is generated and utilized within a business. ANZ Bank and Commonwealth Bank use these methods in their financial reporting to reflect their cash management practices.

Direct Method: Report monetary inflows and outflows directly. It shows consumer cash receipts and supplier and staff cash payments. Their latest financial statements:

• ANZ Bank received AUD 84 billion from consumers and paid AUD 64 billion to suppliers and staff.

• Commonwealth Bank reported AUD 90 billion in client cash receipts and AUD 72 billion in payments.

The direct method gives a straightforward picture of cash flow activities and is useful for assessing operational efficiency.

Indirect Method: Net income is adjusted for non-cash items and working capital adjustments. Net income is reconciled to operating cash flow. For instance:

• ANZ Bank showed a net income of AUD 7.1 billion with adjustments for depreciation and changes in working capital leading to an operating cash flow of AUD 6 billion.

• Commonwealth Bank had a net income of AUD 10.2 billion, with adjustments resulting in an operating cash flow of AUD 9 billion.

.png)

Figure 1: Triple Bottom Line

(Source: Environmentenergyleader, 2023)

CSR Activities and Triple Bottom Line: Commonwealth Bank and ANZ Bank value CSR and Triple Bottom Line. ANZ Bank invested AUD 200 million in community and environmental efforts, while Commonwealth Bank invested AUD 250 million in CSR for sustainability and community development. Both banks prioritise social, environmental, and financial performance.

.png)

Figure 2: Global Reporting Initiative

(Source: Sagesustainability, 2021)

Global Reporting Initiative (GRI): Both banks report sustainability using GRI standards. Sustainability reports from ANZ Bank follow GRI principles, covering its environmental and social activities. GRI-compliant Commonwealth Bank highlights its carbon emission reduction and diversification efforts.

The financial ratio analysis of ANZ Bank and Commonwealth Bank reveals significant differences in profitability, efficiency, and liquidity. Commonwealth Bank outperforms ANZ Bank in key profitability ratios, including Return on Equity (14.1% vs. 10.1%), Return on Assets (0.81% vs. 0.64%), and Net Profit Margin (12.5% vs. 7.3%), indicating stronger financial performance and better value creation for shareholders. While ANZ Bank shows a slightly higher Asset Turnover Ratio (0.09 vs. 0.07), this minor advantage is overshadowed by Commonwealth Bank’s superior profitability metrics. In terms of liquidity, Commonwealth Bank demonstrates a clear edge with a Current Ratio of 1.53 and a Quick Ratio of 1.05, reflecting a strong ability to meet short-term obligations. ANZ Bank's liquidity ratios are notably weaker, with a Current Ratio of 0.14 and a Quick Ratio of 0.01, signaling potential financial instability. This analysis implies that out of the two, Commonwealth Bank is more preferred because of the fairly higher profitability and better liquidity which means the organization is more financially sound.

Ahmadullo o’g’li, S.K., 2023. INTERPRETING CASH FLOW RATIOS: METRICS FOR ASSESSING FINANCIAL HEALTH. QO ‘QON UNIVERSITETI XABARNOMASI, 9, pp.254-256.

Environmentenergyleader, 2023. Corporate Responsibility in 2023: Triple Bottom Line Sustainability. Available at: https://www.environmentenergyleader.com/2023/02/triple-bottom-line-sustainability/ [Accessed on: 28.08.2024]

Hamadneh, N., Saleh, M., Jawabreh, O., Tahir, M., Al Omari, R. and Shniekat, N., 2021. The Effect of Artificial Intelligence (AI) on the Quality and Interpretation of Financial Statements in the Hotels Classified in the AQABA Special Economic Zone (ASEZA).

Haralayya, B., 2021. Ratio Analysis at NSSK, Bidar. Iconic Research And Engineering Journals, 4(12), pp.170-182.

Lee, H., Cashin, A.G., Lamb, S.E., Hopewell, S., Vansteelandt, S., VanderWeele, T.J., MacKinnon, D.P., Mansell, G., Collins, G.S., Golub, R.M. and McAuley, J.H., 2021. A guideline for reporting mediation analyses of randomized trials and observational studies: the AGReMA statement. Jama, 326(11), pp.1045-1056.

Lim, W.M. and Kumar, S., 2024. Guidelines for interpreting the results of bibliometric analysis: A sensemaking approach. Global Business and Organizational Excellence, 43(2), pp.17-26.

Mann, N., Spencer, G., Hutchinson, B., Ngongo, C., Tarlton, D., Webb, D., Grafton, D. and Nugent, R., 2024. Interpreting results, impacts and implications from WHO FCTC tobacco control investment cases in 21 low-income and middle-income countries. Tobacco Control, 33(Suppl 1), pp.s17-s26.

Olayinka, A.A., 2022. Financial statement analysis as a tool for investment decisions and assessment of companies’ performance. International Journal of Financial, Accounting, and Management, 4(1), pp.49-66.

Sagesustainability, 2021. GLOBAL REPORTING INITIATIVE. Available at: https://sagesustainability.in/global-reporting-initiative/ [Accessed on: 28.08.2024]

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2022. Financial accounting theory and analysis: text and cases. John Wiley & Sons.

Wsj, 2024. ANZ Group Holdings Ltd. Available at: https://www.wsj.com/market-data/quotes/au/xasx/ANZ [Accessed on: 28.08.2024]

Wsj, 2024. Commonwealth Bank of Australia. Available at: https://www.wsj.com/market-data/quotes/au/CBA [Accessed on: 28.08.2024

Essay: 10 Pages, Deadline: 2 days

They delivered my assignment early. They also respond promptly. This is excellent. Tutors answer my questions professionally and courteously. Good job. Thanks!

![]() User ID: 9***95 United

States

User ID: 9***95 United

States

Report: 10 Pages, Deadline: 4 days

After sleeping for only a few hours a day for the entire week, I was very weary and lacked the motivation to write anything or think about any suggestions for the writer to include in the paper. I am glad I chose your service and was pleasantly pleased by the quality. The paper is complete and ready for submission to the professor. Thanks!

![]() User ID: 9***85 United

States

User ID: 9***85 United

States

Assignment: 8 Pages, Deadline: 3 days

I resorted to the MBA assignment Expert in the hopes that they would provide different outcomes after receiving unsatisfactory results from other assignment writing organizations, and they genuinely are fantastic! I received exactly what I was looking for from this writing service. I'm grateful.

![]() User ID: 9***55

User ID: 9***55

Assignment: 13 Pages, Deadline: 3 days

Incredible response! I could not believe I had received the completed assignment so far ahead of the deadline. Their expert team of writers effortlessly provided me with high-quality content. I only received an A because of their assistance. Thank you very much!

![]() User ID: 6***15 United

States

User ID: 6***15 United

States

Essay: 8 Pages, Deadline: 3 days

This expert work was very nice and clean.expert did the included more words which was very kind of them.Thank you for the service.

![]() User

ID: 9***95 United

States

User

ID: 9***95 United

States

Report: 15 Pages, Deadline: 5 days

Cheers on the excellent work, which involved asking questions to clarify anything they were unclear about and ensuring that any necessary adjustments were made promptly.

![]() User ID: 9***95 United

States

User ID: 9***95 United

States

Essay: 9 Pages, Deadline: 5 days

To be really honest, I can't bear writing essays or coursework. I'm fortunate to work with a writer who has always produced flawless work. What a wonderful and accessible service. Satisfied!

![]() User ID: 9***95

User ID: 9***95

Essay: 12 Pages, Deadline: 4 days

My essay submission to the university has never been so simple. As soon as I discovered this assignment helpline, however, everything improved. They offer assistance with all forms of academic assignments. The finest aspect is that there is also an option for escalation. We will get a solution on time.

![]() User ID: 9***95 United

States

User ID: 9***95 United

States

Essay: 15 Pages, Deadline: 3 days

This is my first experience with expert MBA assignment expert. They provide me with excellent service and complete my project within 48 hours before the deadline; I will attempt them again in the future.

![]() User ID: 9***95 United

States

User ID: 9***95 United

States