ACCM4300 Financial Reporting Report 4

You are required to prepare a business letter to address key accounting issues in regards to an acquisition analysis of a wholly owned subsidiary and various intragroup transactions. Also, provide advice on accounting for a foreign currency transaction. This is an individual assessment.

Assume that you are a graduate accountant working for Wolfram Hart, a public accounting firm situated at 388 Ann Street, Brisbane, QLD 4000. The Manager of your firm, Ms. Lily Morgan,has asked you to prepare a statement of advice in response to an email received from a client, Maddie Shannon, the Managing Director of Tottoys Ltd, raising several accounting issues.

Please refer to the email on the next page.

The maximum length for the body of the letter is 2,000 words. You should address all the technical issues and discussion in your advice, followed by a Reference List.

• Part A: Technical component 25% - This mark covers the technical content of your advice and the explanation of each of the issues, the calculations and journal entries (where applicable).

• Part B: Communication Skills 15% - This mark covers the generic skills of writing; layout, clear meaning, structure and organisation, appropriate tone and grammar, spelling, and punctuation throughout the whole assignment. It also includes referencing.

Name

Graduate Accountant

Wolfram Hart

388 Ann Street

Brisbane, QLD 4000

17/02/2025

Ms. Maddie Shannon

Managing Director

Tottoys Ltd

246 Rubik’s Road

Melbourne 3000

Subject: Statement of Advice on Accounting Issues for the Year Ended 30 June 2024

Dear Ms. Shannon,

I am honoured to assist you in solving your accounting problems by providing justifications and the necessary journal entries in adherence to the respective accounting standards. This approach aims to enhance performance and provide clear explanations for each accounting transaction. Your accounting challenges are well-defined; therefore, to structure comprehensive recommendations, the key factors and relevant terminologies applicable to each transaction are outlined below.

According to AASB 3 Business Combinations, purchase consideration refers to the total value of all payments made to acquire the target company, which, in this context, is Byte Ltd by Tottoys Ltd.

Regarding the acquisition of Byte Ltd, Tottoys Ltd used a combination of cash and a non-cash method, which involved issuing its own shares in exchange for the remaining 90% of Byte Ltd’s issued shares. The following outlines how different aspects of purchase consideration are defined:

According to the acquisition agreement, Tottoys Ltd proposed to offer $2.20 per share with a view of acquiring the 90,000 shares in Byte Ltd floated by its shareholders. This leads to total cash consideration as follows:

90,000×2.20=198,000

However, it should be noted that in the cash consideration part, the payment was done in two tranches.

• The first instalment to be paid on 1 July 2023 (at the acquisition date) is $ 99,000.

• Second instalment to be paid on 1 July 2024 $ 99,000.

This is a liability in the company’s balance sheet when the acquisition was affected since this is an obligation to pay in the future.

From an accounting perspective, AASB 3 Business Combinations states that consideration payable in the future should be identified at its market value on the acquisition date. However, in this case, since the payment will be made in one-year instalments, there is no significant need for discounting. The entire amount of $99,000 is recorded as a liability in Tottoys Ltd’s accounts under 'Acquisition Payable’.

Apart from the cash consideration, Tottoys Ltd also paid for the consideration with the company’s shares. It was stated that for every three ordinary shares in Byte Ltd, the shareholders would be entitled to one ordinary share in Tottoys Ltd.

Number of newly purchased shares = 9,000.

Ownership percentage of Byte Ltd = 90%.

Total number of shares owned by the shareholders = 90,000 shares.

To complete the exchange transaction the shareholders of Tottoys Ltd will be issued with Byte Ltd shares in the ratio of 1 share of Tottoys Ltds for every 3 shares of Byte Ltd.

Total share issued = 90,000÷3=30,000 shares

At the time of the acquisition, the Tottoys Ltd shares were quoted at one hundred and sixty dollars per share thus the fair total value of all the issued shares is.

30,000×1.60=48,000

As stated in AASB 3, the beneficial interest element is evaluated at its fair value on the purchase date if equity instruments are issued as consideration (AASB.GOV.AU, 2025). Consequently, in the books of Tottoys Ltd, $48,000 is recorded as an increase in share capital, which is determined by adding the cash receipts from issuing new shares to the balance of the share capital account.

The real value passed in the share exchange transaction to acquire Byte Ltd is the total of:

.png)

According to AASB 3.39, any deferred cash payment must be classified as a liability in the company’s balance sheet as of the acquisition date. The second installment of $99,000 is recorded under 'Acquisition Payable' on Tottoys Ltd’s balance sheet.

.png)

According to AASB 3 Business Combinations, all separately identifiable assets obtained in a business combination should be determined at fair value as of the acquisition date (AASB 3.18) (AASB.GOV.AU, 2025). This means that the equipment for MBA assignment expert should be reported at its fair value of $34,000 rather than it carrying amount of $27,000.

However, since the revised estimate of the consumable items' useful life is only two years, additional depreciation must be accounted for in accordance with AASB 116 Property, Plant and Equipment.

In order to record the fair value adjustment there is a need to perform the following steps:

Observe that the asset’s carrying amount was $27,000, and the revaluation increase is $7,000, so that the carrying amount is increased to $34,000.

Understand the nature of revaluation surplus as stated under AASB 3.18 and AASB 116.31, where it specifies that the revaluation is taken directly in retained earnings or in goodwill (AASB.GOV.AU, 2025).

.png)

Accounting adjustments for “Quantumblox ™”

When Tottoys Ltd acquired this patent, it assigned a fair value of $20,000, meeting the requirements for business combinations. According to AASB 3 Business Combinations (paragraphs 10 & 18), specific and identifiable intangible assets, such as patents, must be recognized separately from goodwill when their fair value can be determined reliably.

AASB 138 Intangible Assets says that intangible asset (for instance, a patent) is recognized if:

• It is separable, i.e., it can be disconnected from contractual / legal rights.

• It is even likely that such benefits as economic gains will accrue to the entity.

• It is also reliable for measurement at fair value (AASB 138.21) (AASB.GOV.AU, 2025).

Since the above criteria have been met, and with the given fair value estimate of $20000, the patent will be regarded as an intangible asset in the consolidated financial statements.

.png)

Dr Intangible Assets – Patent ($20,000): This is recorded under AASB 3.10 and AASB 138.21 intangible asset register as the patent has been valued at this figure during purchase.

Cr Business Combination Gain (or Goodwill Reduction) ($20,000)

This entry is made when analysing the acquisition and is only recorded if goodwill is recognized under the acquisition method. If the business combination outcomes in a bargain purchase, goodwill is reduced accordingly

Accounting for the liability to Employees as per GRIA for $25000

Byte Ltd has disclosed that some of its salaried employees have been underpaid, leading to potential litigation. While the outcome remains uncertain, independent forecasters estimate that $25,000 will be required as a provision.

As directed by AASB 137 Provisions, Contingent Liabilities, and Contingent Assets, a provision must be established when there is a existing obligation, a probable outflow of cash, and a reliable estimate of the cost (Ward, 2023). Since Byte Ltd’s liability meets these criteria, the provision is recognized. Additionally, AASB 3 Business Combinations states that liabilities at the acquisition date must be measured at their fair value.

Journal entry on 1 July 2023 is:

.png)

This entry reflects the legal requirement and confirms that the liability has been accounted for in Tottoys Ltd’s consolidated financial statements. This treatment aligns with AASB 137 and AASB 3, ensuring an accurate representation of the company's financial position in the post-acquisition context (AASB.GOV.AU, 2025).

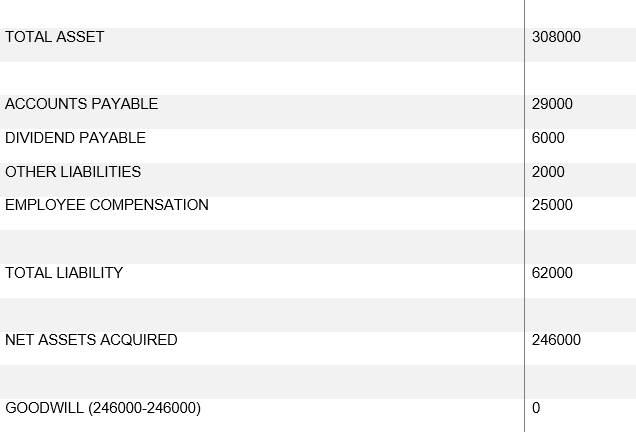

1. Net value of assets Acquired

In the given case, the scenario after calculating the net assets acquired at the fair value after adjusting the liabilities is $246000 which is like the value which is being paid as consideration.

2. Calculation of Goodwill

Goodwill is calculated as the distinction between the purchase consideration paid and the net value of total assets bought after adjusting for liabilities (Das, 2024).

Goodwill represents the additional of the acquisition cost over the actual net value of the acquired assets. It is an intangible asset that reflects the expected benefits from synergies, brand reputation, customer loyalty, operational efficiencies, and other factors that cannot be separately identified or measured individually.

However, in this case, since the purchase consideration paid for Byte Ltd equals the total value of the acquired assets, no additional goodwill needs to be recognized. Instead, the existing goodwill recorded in Byte Ltd’s books can be consolidated as goodwill in Tottoys Ltd.’s financial statements.

Adjustment for assets and Liabilities

.png)

According to AASB 3 Business Combinations, goodwill is recognized in business combinations but cannot be pay back. As an alternative, it must be tested for impairment yearly or whenever there are indications of a decline in value

As per AASB 10, intercompany transactions and associated profits should be eliminated during the consolidation process, as consolidation reflects the economic operations of the group as a single entity.

In this regard, since Byte Ltd has sold 70% of the goods, the profit on those sales can be recognized. However, the remaining 30% of goods still in Byte Ltd’s inventory is considered unrealized and must be written off.

The profit arising from intercompany sales should be adjusted in the consolidated profit to ensure that only realized profit is recognized when goods are sold to a third party. Since 30% of Byte Ltd.'s remaining inventory has not been sold externally, the intercompany profit on these goods must be eliminated. This unrealized profit should be removed from the consolidated accounts to reflect the value that would have been realized if all assets had been sold. Here’s how you would proceed

They should also cost it down for the unsold inventory by removing Unrealized Profit for the Unsold Goods – 30%.

It is important that for the consolidated financial statements, the unrealized profit from the unsold inventories should be adjusted out. Since Byte Ltd. sold only 70% of the products, 30% of the profit per item remains untapped.

Its Unrealized Profit to Eliminate means that 30% of $12,000 =$36000.

.png)

AASB 10 – Consolidated Financial Statements: Elimination of intercompany transactions: Sales and profits which occur between entities of affiliated companies must be eliminated.

AASB 3 Business Combinations: When consolidating, gains that have not otherwise been entered into the current period through external sales need to be eliminated.

AASB 116 – Property, Plant & Equipment: Equipment costs are capitalized and there is depreciation with the expense charged in the stating comprehensive income. These costs include cost of installation which is incurred while procuring the asset and increases the overall cost of the asset which is then depreciated for its useful lifetime.

Intercompany sales must be eliminated from the consolidated financial statements, and any gains on these sales should be deferred until the asset involved is used by external entities (Sindonen, 2024). Since Byte Ltd owns the equipment, the depreciation and installation costs recorded by Byte Ltd should be adjusted accordingly in the consolidation process.

Unrealized Profit:

It is important to note that the profit on the sale between Tottoys Ltd and Byte Ltd is yet to be realized hence it will not be consolidated. The profit that must be eradicated in the sale of the equipment is $4,000.

Depreciation and Installation Costs:

Byte Ltd will depreciate the equipment by $700 per year that is 10% of the cost price of $7,000. The installation cost of $1,500 of the equipment is also treating as cost of Byte Ltd.’s equipment.

1. Eliminate Intercompany Profit

The profit, which Tottoys earns from the sale to Byte, is not realised in the consolidated accounts thus eliminating the intercompany profit and adjusting the value of the asset.

.png)

Further at the time of preparing the consolidated financial statement will need adjustment in the depreciation expenses as well.

Accounting adjustments for foreign currency transaction

This case involves a foreign exchange transaction related to a loan issued in USD and expenses incurred for constructing a manufacturing facility. The accounting treatment must comply with AASB 121 The Effects of Changes in Foreign Exchange Rates and other relevant Australian accounting standards. Fluctuations in exchange rates may occur between the time of borrowing, construction, and interest payments. Therefore, any variations resulting from changes in exchange rates must be appropriately accounted for (Standard, 2024).

AASB 121 states that foreign exchange changes on foreign currency loans should be predictable in the profit and loss account, except when the loan is selected as a hedging tool, in which case the difference should be recorded in other comprehensive income.

In this case, if no hedging has been applied, foreign exchange gains or losses arising from the translation of foreign currency into the domestic currency will be added to or removed from the profit or loss statement.

Since no significant information is available regarding foreign currency transactions or translation-related differences, no additional adjustments are required beyond the recognition of the loan and its associated investment.

In response to the queries you have raised, we have provided all relevant information in agreement with the appropriate accounting standards to ensure better representation and understanding of the transactions. However, these transactions are not intended to be posted into the financial statements, as additional information may be required

Regards,

AASB.gov.au 2025. Business combinations. Available at: https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15_COMPjun20_01-22.pdf (Accessed: 11 February 2025).

AASB.GOV.AU 2025. Compiled AASB 10 (December 2021). Available at: https://aasb.gov.au/admin/file/content105/c9/AASB10_07-15_ACOMPdec21_01-22.pdf (Accessed: 11 February 2025).

AASB.GOV.AU 2025. Property, plant and equipment. Available at: https://www.aasb.gov.au/admin/file/content105/c9/AASB116_08-15_COMPdec16_01-19.pdf (Accessed: 11 February 2025).

Das, P.K., 2024. Accounting for Intangible Assets, a Study. Management, 4(5), pp.147-155. https://kspublisher.com/media/articles/MERJEM_45_147-155.pdf

Sindonen, E. 2024. Implementation of Intercompany Reconciliation. https://www.theseus.fi/bitstream/handle/10024/853946/Sindonen_Ekaterina.pdf?sequence=2

Standard, A. A. S. B. 2024. Presentation and Disclosure in Financial Statements. https://aasb.gov.au/admin/file/content105/c9/AASB18_06-24_AmendStd.pdf

Ward, J. 2023. Contingent liabilities: Contingent liabilities and solvency. Australian Restructuring Insolvency & Turnaround Association Journal, 35(3), 28-31. https://search.informit.org/doi/pdf/10.3316/informit.320047193548285

Essay: 10 Pages, Deadline: 2 days

They delivered my assignment early. They also respond promptly. This is excellent. Tutors answer my questions professionally and courteously. Good job. Thanks!

![]() User ID: 9***95 United

States

User ID: 9***95 United

States

Report: 10 Pages, Deadline: 4 days

After sleeping for only a few hours a day for the entire week, I was very weary and lacked the motivation to write anything or think about any suggestions for the writer to include in the paper. I am glad I chose your service and was pleasantly pleased by the quality. The paper is complete and ready for submission to the professor. Thanks!

![]() User ID: 9***85 United

States

User ID: 9***85 United

States

Assignment: 8 Pages, Deadline: 3 days

I resorted to the MBA assignment Expert in the hopes that they would provide different outcomes after receiving unsatisfactory results from other assignment writing organizations, and they genuinely are fantastic! I received exactly what I was looking for from this writing service. I'm grateful.

![]() User ID: 9***55

User ID: 9***55

Assignment: 13 Pages, Deadline: 3 days

Incredible response! I could not believe I had received the completed assignment so far ahead of the deadline. Their expert team of writers effortlessly provided me with high-quality content. I only received an A because of their assistance. Thank you very much!

![]() User ID: 6***15 United

States

User ID: 6***15 United

States

Essay: 8 Pages, Deadline: 3 days

This expert work was very nice and clean.expert did the included more words which was very kind of them.Thank you for the service.

![]() User

ID: 9***95 United

States

User

ID: 9***95 United

States

Report: 15 Pages, Deadline: 5 days

Cheers on the excellent work, which involved asking questions to clarify anything they were unclear about and ensuring that any necessary adjustments were made promptly.

![]() User ID: 9***95 United

States

User ID: 9***95 United

States

Essay: 9 Pages, Deadline: 5 days

To be really honest, I can't bear writing essays or coursework. I'm fortunate to work with a writer who has always produced flawless work. What a wonderful and accessible service. Satisfied!

![]() User ID: 9***95

User ID: 9***95

Essay: 12 Pages, Deadline: 4 days

My essay submission to the university has never been so simple. As soon as I discovered this assignment helpline, however, everything improved. They offer assistance with all forms of academic assignments. The finest aspect is that there is also an option for escalation. We will get a solution on time.

![]() User ID: 9***95 United

States

User ID: 9***95 United

States

Essay: 15 Pages, Deadline: 3 days

This is my first experience with expert MBA assignment expert. They provide me with excellent service and complete my project within 48 hours before the deadline; I will attempt them again in the future.

![]() User ID: 9***95 United

States

User ID: 9***95 United

States